The recent spate of low oil prices is only partially due to US fracking. The rest is mostly OPEC leaving their production rates high to deliberately force oil prices low. The motivation is two-fold: (1) trying to force US frackers out of the business with prices too low to support that activity, and (2) fear of losing market share as an individual country, if any of them do cut back.

I was surprised and pleased to learn that there really was shale oil producible by fracking. What they appear to be recovering is a "light sweet crude" that actually resembles diesel fuel in its physical properties. This is unlike most crudes, which are much thicker and less mobile, and far less volatile. That volatility is the source of the dangers experienced while shipping this stuff by rail, because there aren't enough of the safer pipelines.

The shales in south Texas are producing this kind of crude, and also the Williston basin formations, most notably in Wyoming. I have seen no figures on what percentage of the hydrocarbons in the rock pores are being recovered, but I'd still bet it's single digit, or not much better. It's just a rich enough set of resources to make recovery feasible, as long as prices are not too low.

The fundamental side effect we are incurring is used frack water. It comes back as a concentrated brine contaminated with heavy metals, other mineral poisons (like arsenic), leftover cancer-causing hydrocarbons (like benzene) from the frack fluid additives, and radioactivity leached from the deep rocks.

No one is re-using this fluid, and there is really not enough fresh water around to fill the demand. Plus, deep well injection disposal is causing earthquakes in north Texas and in Oklahoma, at least. Long term, the solution is obviously re-using frack water (reducing demand on limited supplies of fresh water, and greatly reducing the disposal quantities). That will require developing an additive package that works in brine (which makes sea water feasible as a feedstock source). I can think of nothing that should not be higher on DOE's R&D list.

There are still strong conflicts over whether fracking pollutes ground water. My hunch is that they'd better look closer at the geology in which they frack, and also at well casing quality. Eliminate cheap leaky well casings, and the only other way for natural gas to surface (besides the well) is directly through the rocks. Rock layers that are relatively unfolded and unbroken won't leak very badly. Fractured, folded rocks in mountainous zones will leak very badly. It may well be that simple.

--- GW

Update 1-3-15 at bottom in black.

Updates 2-4-14 below in blue.

Update 6-5-2016 in purple:

I went and looked up a US oil production history curve similar to the one I saw from the 2009 "Science" article used in the article below. I inserted it below adjacent to the older plot for easy comparison. With another 5 years' of history, it is pretty easy to see the Hubbert curve shape in the conventional oil recovery history of US production up to about 2011, and that the Alaska "bump" is actually a fairly small effect.

The fracking technology is a larger effect than I believed at the time. It is a fundamentally new and different production technology, which makes both new shale resources available, and more recovery feasible from older depleted fields. This is a very steep rise ion production, with very little time history yet to interpret trends. It is premature to judge yet, but the steep rise does suggest the narrower Hubbert curve shape of a smaller volume to be recovered.

The Saudis more-or-less lead OPEC in production quotas and prices, but are adversarial with Iran, who is reentering the mass market. All the OPEC countries are afraid of losing market share if they cut back, but are being hurt by lower prices. Yet if they continue to hold prices down by over-production, they may cut off the US fracking boom, which is a fundamentally more expensive technique. We'll see, but the verdict won't come for some years yet.

----------------------------------------------------------------------------------------------------------

By putting together facts from different sources, adding in some events from recent history, and a little common sense, one can draw some startling conclusions. These should make you as mad as they do me. It’s hard to argue with factual data. My conclusions are my own opinions. You draw conclusions for yourself, and form your own opinions.

I start with a graph of US regular gasoline price history from about 1970 to the present, adjusted for inflation, as January 2011-dollar equivalent. I got this from “zfacts.com”, which has quite the variety of both facts and opinions. Price history is fact, not opinion, however.

To this time history graph, I added several historical events, a line representing the current equivalent of 1958’s 25 cent/gallon gasoline, and a second line representing a conclusion I drew from all this data regarding recessions. That modified chart is complicated and takes a while to digest, but here it is:

I was able to discern several connections between this price history and contemporary events, as well as linkages between fuel prices and recessionary events. These are listed in bullet form on the next graphic. The most important one is in capital letters. It makes liars out of most US politicians running for office, from either party. The notion of an enormous monopoly-cartel pricing effect superposed on top of a basic supply-demand price level, makes liars out of those who claim the international oil market is nothing but a “free market”, for it most clearly is not. There is also a price speculation effect superposed on top of supply-and-demand effects. The scariest bullet is the very last one, however.

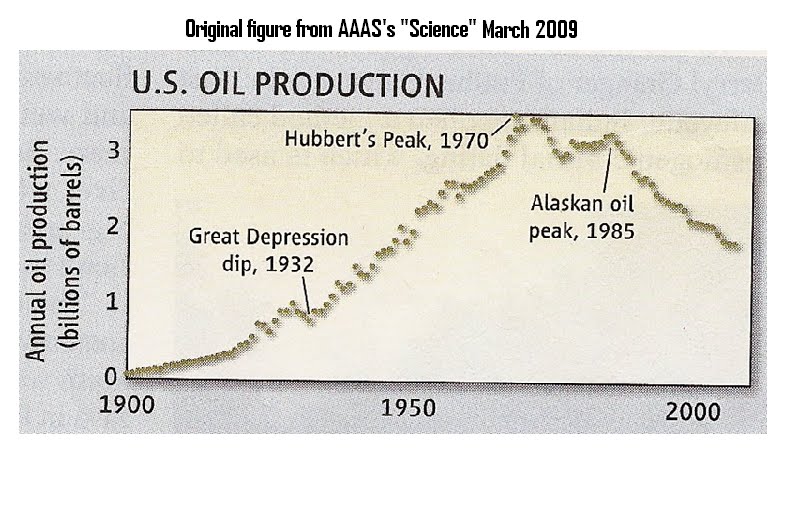

That brings up the question of oil supplies available. Here’s the US production history (actual data):

M. King Hubbert was the geologist who used an empirical curve fit to predict a US production peak in 1965 or 1970, back in 1956. His model takes advantage of a convenient mathematical curve shape, with no scientific causality built in, but was surprisingly accurate. He did this long before oil was discovered in Alaska. The effect of the new oil boom in "the Bakken" is another, larger hump (not shown) on the otherwise-decreasing overall trend. Its effects have temporarily reversed US production to a rise, but it is only temporary. The area under a Hubbert bell curve is proportional to the volume of the resource it models. Here is what that production history looks like with some Hubbert curves superimposed:

My conclusions follow:

---------------------------------------------------------

Update 6-5-2016: Later version of US production history from US EIA website, with Hubbert curve fit sketched upon it by me.

Note how different the fracking trend is, reflecting how fundamentally-different that recovery technology really is. Note also how the sharp rise suddenly cuts off right at the end of the data. The meaning of this is unclear at best. A logical question: how long will this boom last? Hubbert curves for smaller resource volumes tend to be narrower in time, looking "peaky".

------------------------------------------------------

In my opinion this makes (1) liars out of the US politicians running for office who told us we could drill our way out of dependence on foreign oil, and (2) fools out of those who believed them. The new oil boom has reversed this, but remember, that will be temporary!

The depletion of US oil reserves brings up the question of world oil depletion, and its effect on the basic supply-demand pricing level underneath the monopoly cartel pricing effects. The Saudis have not exceeded their own 2004 production levels. They sit on the 3 largest known remaining oil reserves left on the planet. It isn’t pretty:

But wait, some say we have tremendous reserves here at home. I see this claim quite a lot in email forwards about “the Bakken”, and some other names. These forwards always claim we have “cheap oil” in quantities exceeding Saudi Arabia, it’s just that the political opposition and/or environmentalists “won’t let us drill it”. These are just politically-motivated hit pieces. They mix facts with egregious lies and very slanted rhetoric. The truth is quite different. Bulletized list follows. I might add that the cleanup costs for the wastewater generated by the Alberta tar sands products we buy, are not in the product prices we pay, because they are as yet unknown. The volume of wastewater impounded under armed guard now exceeds Lake Erie. No one knows how to clean it up. That bill will come due. Soon.

Update: 3-5-13: Not long after I wrote this came word of a regional oil boom in the Williston Basin. They are using fracking in a thin dolomite layer sandwiched between Bakken shales to get a light crude. I documented this in a later article. Go see 9-5-11 "Surprise Surprise: Oil Boom in the Williston Basin (the "Bakken")". It's a small resource compared to the shales, which still refuse to yield oil.

Update 6-5-2016: the new fracking technology includes shale oil from "the Bakken", the south Texas oil shales, and more. See updated production history plot above.

So, as long as we use oil for fuel, we’re stuck with importing it. Most of those imports come from OPEC, dominated by middle eastern countries, some of whom are downright hostile. What do they do with all that money we have paid them for oil, for the past half century? You won’t like the answer:

We’ve been paying them to kill us. For decades. That does bring up good questions about treason.

There are a lot of entrenched interests long opposed to the implementation of alternative liquid transportation fuels, for a lot of “good-sounding” reasons. Yet there only three types of fuel to worry about, and three good drop-in alternatives available at one level or another, right now.

Gasoline can be stretched quite a bit further by blending-in significant ethanol, without any vehicle or infrastructure modifications (steel and neoprene are as good with ethanol as they are with gasoline). The only relevant questions are what source(s) do we use, and how much is available?

One of the specious arguments against ethanol is the effect of corn diversion from food use to fuel production. Many claim that the upsurge in food prices in 2009 was due to ethanol production. If you look at the actual facts, you find this claim is a lie.

To use ethanol successfully, we need the cellulosic technology that is just now being scaled-up and industrialized. This was originally made possible by grants from NREL, the alternative energy lab that has been part of DOE since Jimmy Carter’s time as president. Those first NREL grants made the industrial R&D possible, that in turn has recently led to pilot plant production of cellulosic ethanol at prices similar to gasoline, or cheaper. (That NREL/DOE story makes liars out of the authors of popular e-mail forwards claiming DOE has been a worthless waste, does it not?)

The situation is similar for using biodiesels in diesel fuel and jet fuel. The algae technology needs its development finished, so it can also be scaled up and industrialized. There’s more of it available.

OK, given that we finish the development, scale-up, and deployment of cellulosic ethanol and algae oils, what could we do with them? Remember, blend fuel products based on these materials are drop-in fuels, suitable even for the legacy fleets of old cars, old trucks, and old airplanes.

Answer: displace as much as possible of that imported oil we get from generally-hostile and financially-predatory OPEC. That picture still obtains, once the new oil boom fades.

If we go for E-33 and B-33 blend levels in the three fuels, this is what could happen:

The US could zero-out the imports it needs from OPEC! Wow!

If the US eliminates its dependence on OPEC oil, that is a major blow to the money OPEC funnels to the terrorists and proxy armies we fight, the US being their single largest customer by far. That has the added benefit of dropping oil prices via the supply-demand mechanism, compounding the denial of funds to the enemy. The rise of demand from rapidly-industrializing China and India has offset this; won't really happen.

If the rest of the western world followed suit, they and we together could dry up virtually all income to the Arab states of OPEC. Since those states have no other source of revenue (they have no other export the world wants), they would have to civilize themselves and join modern society as responsible members, or else go back to the stone age. And they know that (it is their greatest fear)! These nations can still be hurt if everybody just buys much less of their oil. Stretching fuel supplies with alternatives makes that happen, "Bakken" oil boom or not.

In other words, we could win this war economically, with no more invasions or armies. And, start making our economies proof against any more oil price-induced recessions, to boot.

Update 1-3-15:

The recent explosion of US “fracking” technology (hydraulic

fracturing plus horizontal-turn drilling) has modified the picture of oil

prices versus recessions.

Unexpectedly, the US has become a

leading producer of crude oils for the world market. Plus,

there has been an associated massive production increase and price drop

in natural gas.

OPEC has chosen to take the income “hit” and not cut back

their production in response. Their

reasoning is twofold: (1) fear of loss

of market share, and (2) hope that low

oil prices will curtail US “fracking” recoveries. We will see how that plays-out.

Oil prices are now such (at around $55/barrel) that US

regular gasoline prices are nearing $2.00/gal for the first time in a very long

time. This is very close to the price

one would expect for a truly competitive commodity, based on 1958 gasoline prices in the US, and the inflation factor since then.

It is no coincidence that the exceedingly-weak US “Great Recession”

recovery has suddenly picked up steam.

The timing of the acceleration in our economic recovery versus the

precipitous drop in oil prices is quite damning. There can be no doubt that

higher-than-competitive-commodity oil prices damage economies. Oil prices are a superposition of the competitive

commodity price, overlain by an erratic

increase from speculation, and further overlain

quite often by punitive price levels when OPEC is politically unhappy with the

west. That’s been the history.

This economic improvement we are experiencing will persist

as long as oil, gas, and fuel prices remain low. (Government policies have almost nothing to

do with this, from either party.) How long that improvement continues depends

in part upon US “fracking” and in part upon OPEC. Continued US “fracking” in the short term may

depend upon adequate prices. In the long

term, we need some solutions to some

rather intractable problems to continue our big-time “fracking” activities.

The long-term problems with “fracking” have to do with (1)

contamination of groundwater with combustible natural gas, (2) induced earthquake activity, (3) lack of suitable freshwater supply to

support the demand for “fracking”, and

(4) safety problems with the transport of the volatile crude that “fracking”

inherently produces.

Groundwater

Contamination

Groundwater contamination is geology-dependent. In Texas,

the rock layers lie relatively flat,

and are relatively undistorted and unfractured. This is because the rocks are largely old sea

bottom that was never subjected to mountain-building. We Texans haven’t seen any significant

contamination of ground water by methane freed from shale. The exceptions trace to improperly-built

wells whose casings leak.

This isn’t true in the shales being tapped in the

Appalachians, or in the shales being

tapped in the eastern Rockies. There the

freed gas has multiple paths to reach the surface besides the well, no matter how well-built it might have

been. Those paths are the vast

multitudes of fractures in the highly-contorted rocks that subject to mountain-building

in eons past. That mountain-building may

have ceased long ago, but those cracks

last forever.

This is why there are persistent reports of kitchen water

taps bursting into flames or exploding,

from those very same regions of the country. It’s very unwise to “frack” for gas in that

kind of geology.

Induced Earthquake

Activity

This does not seem to trace to the original “fracking”

activity. Instead it traces rather

reliably to massive injections of “fracking” wastewater down disposal

wells. Wherever the injection quantities

are large in a given well, the frequent

earthquakes cluster in that same region.

Most are pretty weak, under

Richter magnitude 3, some have

approached magnitude 4.

There is nothing in our experience to suggest that magnitude

4 is the maximum we will see. No

one can rule out large quakes. The risk is with us as long as there are

massive amounts of “fracking” wastewater to dispose of, in these wells. As long as we never re-use “frack”

water, we will have this massive

disposal problem, and it will induce

earthquakes.

Lack of Freshwater

Supply to Support “Fracking”

It takes immense amounts of fresh water to “frack” a single

well. None of this is ever re-used, nor it is technologically-possible to

decontaminate water used in that way. The

additives vary from company to company,

but all use either sand or glass beads,

and usually a little diesel fuel.

Used “frack” water comes back at near 10 times the salinity of sea

water, and is contaminated by heavy

metals, and by radioactive minerals, in addition to the additives. Only the sand or glass beads get left

behind: they hold the newly-fractured

cracks in the rocks open, so that

natural gas and volatile crudes can percolate out.

The problem is lack of enough freshwater supplies. In most areas of interest, there is not enough fresh water available to

support both people and “fracking”, especially

with the drought in recent years. This assessment

completely excludes the demand increases due to population growth. That’s even worse.

This problem will persist as long as fresh water is used for

“fracking”, and will be much, much worse as long as “frack” water is not

reused. The solution is to start with

sea water, not fresh water, and then to re-use it. This will require some R&D to develop a

new additive package that works in salty water to carry sand or glass

beads, even in brines 10 times more

salty than sea water.

Nobody wants to pay for that R&D.

Transport Safety with

Volatile “Frack” Crudes

What “fracking” frees best from shales is natural gas, which is inherently very mobile. Some shales (by no means all of them) contain

condensed-phase hydrocarbons volatile enough to percolate out after hydraulic

fracturing, albeit more slowly than

natural gas. Typically, these resemble a light, runny winter diesel fuel, or even a kerosene, in physical properties. More commonly, shale contains very immobile condensed

hydrocarbons resembling tar. These cannot

be recovered by “fracking” at all.

The shales in south Texas,

and some of the shales and adjacent dolomites in the Wyoming region

actually do yield light, volatile

crudes. The problem is what to transport

them in. There are not enough

pipelines to do that job. Pipelines are safer

than rail transport, all the spills and

fires notwithstanding.

The problem is that we are transporting these

relatively-volatile materials in rail tank cars intended for normal (heavy)

crude oils, specifically DOT 111 tank cars. Normal crudes are relatively-nonvolatile and

rather hard to ignite in accidents. DOT

111 cars puncture or leak frequently in derail accidents, but this isn’t that serious a problem as long

as the contents are non-volatile. These

shale-“frack” light crude materials resemble nothing so much as No. 1 winter

diesel, which is illegal to ship in DOT

111 cars, precisely since it is too

volatile.

The problem is that no one wants to pay for expanding the

fleet of tougher-rated tank cars. So, many outfits routinely mis-classify “frack” light

crudes as non-volatile crudes, in order

to “legally” use the abundant but inadequate DOT-111 cars. We’ve already seen the result of this kind of

bottom line-only thinking, in a series

of rather serious rail fire-and-explosion disasters, the most deadly (so far) in Lac

Megantic, Quebec.

Volatile shale-“fracked” crudes simply should not be shipped

in vulnerable DOT 111 cars, period. It is demonstrably too dangerous.

Conclusions

“Fracking” shales for natural gas and light crudes has had a

very beneficial effect on the US economy and its export-import picture. We should continue this activity as a

reliable bridge to things in the near future that are even better.

But, we must address

the four problem areas I just outlined.

And I also just told you what the solutions are. The problem is, as always,

who pays. What is the value of a

human life? What is the value of a

livable environment? It’s not an either-or

decision, it’s striking the appropriate balance!

No comments:

Post a Comment